Understanding the Basics for Estate Taxes

The US imposes estate taxes on assets transferred from the estate of a deceased individual to heirs or beneficiaries. In understanding the basics for estate taxes, an estate tax is not the same as an inheritance tax. It’s a tax on the total value of a person’s assets at the date of death. The estate pays the tax before any assets are distributed to beneficiaries or heirs.

In contrast, inheritance tax is based on the value of assets that an individual beneficiary receives. The tax responsibility is on the beneficiary, not the estate, and tax rates can depend on the relationship between the decedent and the beneficiary.

US Estate Taxes Overview

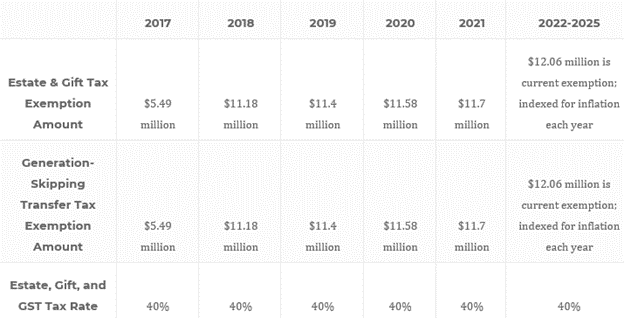

US estate taxes apply only to high-value estates. The amount adjusts annually for inflation, and for 2023 is $12.92 million per individual—higher estate tax exemptions will sunset on December 31, 2025. Projections vary slightly but align with a 2026 estate tax exemption cut in half to about $6.8 million per individual. Any value exceeding the current year’s exclusion limit is subject to tax.

The Internal Revenue Service requires any estate with prior taxable gifts and combined gross assets exceeding the threshold to file a federal estate tax return and pay estate tax. Therefore, any estate valuation in 2023 over $12.92 million per individual will pay tax on the overage amount. Executors, or personal representatives, are responsible for filing the estate’s return and paying any taxes owed by the estate, from the estate, over that year’s exclusion amount.

Unlimited Marital Deduction

A provision in the US Federal Estate and Gift Tax Law allows an individual to transfer an unrestricted amount of assets at any time to their spouse free from tax. This transfer includes the date of death of the transferor.

However, this unlimited deduction from estate and gift tax only postpones the taxes on the property inherited from each other until the second spouse dies. After the surviving spouse’s death, all estate assets over the exclusion amount are subject to the survivor’s taxable estate.

Assets Subject to Estate Tax

The estate tax applies to the fair market value of assets such as cash, real estate, stocks, bonds, and personal property, including art, jewelry, and other collections. Life insurance proceeds paid to a beneficiary are generally not subject to estate tax but may be included in the estate if the deceased owns the policy.

Exemptions and Deductions

Certain deductions and exemptions can help reduce the amount of estate taxes owed. For example, a married couple can pass on their estate to their spouse without incurring estate tax at that time. Additionally, charitable donations made from the estate can qualify as a deduction from the taxable amount.

Reducing Estate Taxes

Estate tax law can be complex, and an estate planning attorney can provide valuable guidance and assistance when minimizing the impact of estate taxes. Here are some ways an estate planning lawyer can help:

- Creating an estate plan minimizes the impact of estate taxes. An estate planning attorney can help you explore various strategies, such as gifting, trusts, and other tax-efficient structures, to reduce the size of your taxable estate.

- Reviewing and updating your estate plan and making revisions every year or so ensures it’s optimized to minimize estate taxes.

- Estate planning strategies can reduce the impact of estate taxes, such as gifting, trusts, and life insurance. These strategies are complex and are customized to each individual’s unique circumstances.

- Ensuring compliance with tax laws and regulations that govern estate taxes ensures you are taking advantage of all available deductions and exemptions.

- Helping to file estate tax returns to ensure all necessary information is included and the return is filed accurately and on time.

- Providing guidance to executors and trustees with a fiduciary responsibility to manage the estate in a way that minimizes taxes and maximizes the value of the assets for heirs and beneficiaries.

An estate planning attorney is a valuable resource for individuals concerned about estate taxes and minimizing their impact.

Estate Taxes by State

In addition to federal estate taxes, some states have their own estate or inheritance taxes. Currently, twelve states levy an estate tax upon your death. Like federal estate tax law, state-level estate taxes can change. There may be additional requirements for exemptions that apply depending on the year. If you are concerned about estate taxes in your state, it’s a good idea to consult with an estate planning attorney for guidance and advice specific to your situation.

Spending Down Your Estate

Reducing the size of your estate can minimize or avoid federal estate tax. Enjoy your wealth if you aren’t afraid of running out of money before you die. Travel, live lavishly, and give your assets to loved ones that may improve their lives while you can enjoy the experience. You can give away your assets to a qualifying charity and deduct them from your estate. Also, you can use an irrevocable trust to shield assets that legally shelter them from federal or state estate taxes. You can even relocate to a more favorable tax environment if you live in a state that levies estate taxes.

Creating a Plan

Your estate planning goals define the steps you take. Establish a clear idea of what you want to happen, to whom you want to give, who will handle your estate, and how estate taxes can be avoided to protect the legacy you leave to your loved ones.

An estate planning attorney can help you gather and organize your financial data to determine your net worth and establish estate tax avoidance strategies, review all existing beneficiary selections, and make updates where appropriate. They help you understand the importance of how you hold title to your property.

Create your estate plan today, knowing you can modify much of it as your family situation changes. Estate taxes may be an important consideration if you have a large estate. By understanding the basics of estate taxes and working with an estate planning attorney, you can ensure your assets transfer to your loved ones in the most tax-efficient manner possible.

This article offers a summary of aspects of estate planning and elder law. It is not legal advice and does not create an attorney-client relationship. For legal advice, contact our Ruston, LA office by calling us at (318) 255-1760.